Opening and operating a small business comes with its rewards as well as a fair share of challenges. Planning for retirement is one of the most critical areas that does not get sufficient attention from small business owners. As an entrepreneur, you have to ensure the business and your personal retirement finances are both well-planned and secured. Fortunately, there are dedicated small business retirement plans which allow you and your team to plan for the future.

This article aims to assess the different retirement plan options that small businesses have, the advantages they confer, and how to determine the right one for your business.

Why Small Business Retirement Plans Are Essential

Small business owners routinely deal with a very specific problem in the landscape of retirement planning. Most small business owners do not have a large company bankrolling them so they have no access to things like a 401(k). When there are no retirement benefits offered, it creates an incentive to ignore planning altogether.

Implementing a retirement plan for your business allows you to save efficiently, reduce tax burden, and helps in attracting and retaining skilled employees.

In addition to that, your employees will surely appreciate the benefits that come along with it. Moreover, it will give you peace of mind to know that you are securing your financial future.

Popular Small Business Retirement Plans

1. SEP IRA (Simplified Employee Pension Individual Retirement Account)

Due to its popularity, a SEP IRA is one of the most common retirement plans for small businesses. This retirement plan works best for sole proprietors and businesses with few employees, here’s why.

- Contributions: As a business owner, you can contribute up to 25% of your employee’s salary (up to a limit of $66,000 in 2025). Plus, contributions are tax-deductible for your business which reduces your taxable income.

- No employee contributions: Employees are not able to make contributions to a SEP IRA, meaning only the employer can contribute. Unlike 401(k) plans, with a SEP IRA there is only employer participation.

- Flexible: The plan can be set up relatively quickly and there are no annual filing requirements. For businesses seeking a straightforward retirement plan, this is an excellent choice.

2. Simple IRA (Savings Incentive Match Plan for Employees)

The Simple IRA Plan is one of the more affordable options for small businesses. In contrast to SEP IRAs, both employers and employees can contribute to a Simple IRA. Here’s why a Simple IRA is a great option for small businesses:

- Employee Contributions: In 2025, your employees may contribute a maximum of 15,500, and those aged 50 and over can make an additional 15,500, catch-up contribution.

- Employer Contributions: As a small business owner, you are required to either match your employee’s contributions up to 3% of their salary or provide a 2% non-elective contribution for each eligible employee.

- Easy to Set Up: The Simple IRA is inexpensive compared to other retirement options because it is simple to set up and administer.

3. Solo 401(k) (Individual 401(k))

Sole proprietors or business owners with one employee, their spouse, and no additional employees may find that a Solo 401(k) is the best option. This plan allows participation both as an employee and employer:

- Employee Contributions: As an employee, your contribution limit in 2025 is 22,500, increasing to 30,000 if you’re 50 or older.

- Employer Contributions: As an employer, you may contribute 25% of your net earnings, not exceeding a total of 66,000 and 73,500 if you’re 50 or older.

- Tax Benefits: There are also tax benefits as a Solo 401(k), which offers tax-deferred growth on investments until withdrawn in retirement.

4. Defined Benefit Plan

A Defined Benefit Plan closely resembles traditional pension schemes, where the employer gives a certain benefit upon retirement. These plans are more intricate, and ideal for larger small businesses looking to provide meaningful retirement benefits to themselves or key employees.

- Guaranteed Payments: In contrast to contribution-based plans like 401(k)s, a defined benefit plan guarantees a specific monthly benefit at retirement, which is determined by factors like salary history and tenure with the organization.

- Contribution Limits: The contribution limits are significantly greater than other plans, with an upper limit of $245,000 in 2025. This greatly benefits business owners earning high incomes and wishing to make significant contributions.

Choosing the Right Small Business Retirement Plan

Entering into a retirement plan for your small business comes with numerous options. Some of these options include the size of the business, budget, and the management level you wish to be involved in. Let us look at some of the things to put in place:

- Employee Size: If your business is small, a SEP IRA or Solo 401(k) are easy and affordable to administer. Other larger establishments would find a Simple IRA more beneficial as it offers greater flexibility compared to a Defined Benefit Plan.

- Budget: More expensive retirement plans such as Defined Benefit Plans incur steep maintenance and setup costs, and are not ideal for those on a budget or looking to keep costs down. Other options like Solo 401(k) or SEP IRA are much easier to manage financially.

- Tax Benefits: Some plans give better tax relief than others. For both parties the retirement plan must give equal benefits. An example is the SEP IRA that has simple contribution clauses compared to the Simple IRA. Solo 401(k) also benefits sole proprietors instilling great savings.

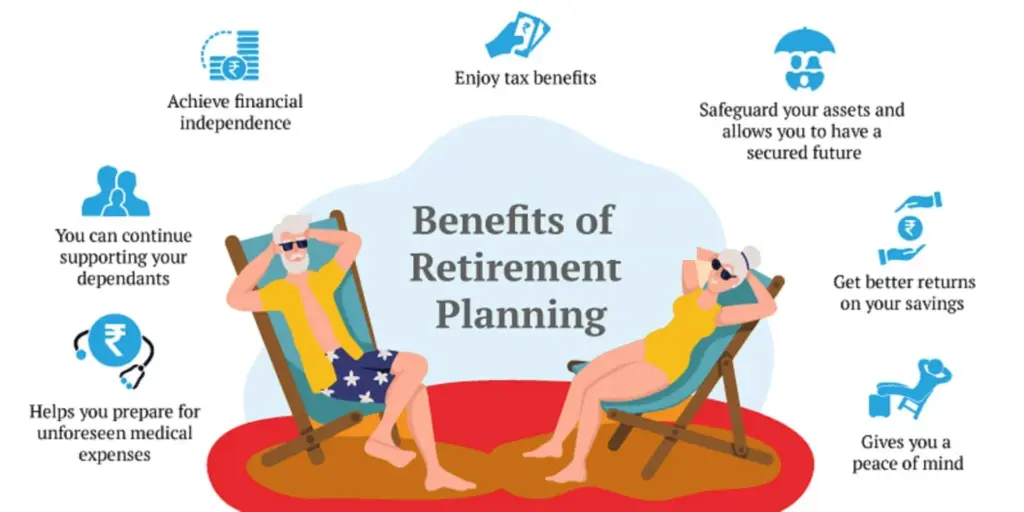

The Benefits of Offering a Retirement Plan

A retirement plan can especially put your business ahead of others in securing the best skilled professionals, and keeps them around for longer periods as they perceive increased company loyalty.

Retirement benefits increase the value of your employee’s services, and offering a retirement plan demonstrates your dedication to their future wellness. Here are some additional advantages of offering a retirement plan:

- Tax Deductions: As an employer, you can claim tax-deductible contributions to your retirement plans, creating a tax-savings for your business.

- Attracting Talent: Competitive businesses often use strong retirement plans as bait to attract new talent into the organization.

- Employee Retention: Employees are more likely to remain with a company that has retirement plans, reducing overall turnover.

Conclusion

If you are a small business owner, consider securing your retirement equally as you would with the daily operational management of the business. The right retirement plan ensures you and your employees are financially secure. Business owners can choose from several options tailored to their businesses such as SEP IRAs, Simple IRAs, or Solo 401(k)s.

After formulating a plan, consult with your financial advisor to see how well your business goals intertwine with the selected plan. Early retirement planning translates to a world of difference in the long-term.